Are you a young professional in Delhi wondering, “Should I spend ₹6,000 on a luxury bag?” A recent Reddit post on AskDelhi sparked this exact debate. A 21-year-old woman, earning ₹63,000 a month, debated buying a discounted GUESS bag but felt guilty due to her family’s past financial struggles. Among the responses, my advice stood out: donate ₹4,000 to someone in need and buy a high-quality, five-star-rated bag for ₹2,000 online. This approach not only saves money but also aligns with smart budgeting and generosity. Here’s why my advice is the best choice for young professionals in Delhi and why overpaying for luxury brands like GUESS is often a trap.

The Hidden Cost of Luxury Bags in Delhi

Luxury brands like GUESS thrive on their name, not necessarily their quality. A ₹6,000 bag may seem like a steal on discount, but is it worth it? Consumer reviews on platforms like Flipkart and Amazon India show that bags priced at ₹1,500–₹2,500 often match luxury brands in durability, style, and functionality. For example, brands like Lavie or Caprese offer stylish, well-reviewed bags with strong stitching and premium materials at a fraction of the cost.

In Delhi, where the cost of living is high (average rent for a 1BHK in areas like Saket is ₹20,000–₹30,000), spending nearly 10% of a ₹63,000 salary on a bag can strain your budget. The Reddit user’s guilt reflects a deeper truth: luxury purchases often prioritize status over value, especially for those new to financial stability. Instead of falling for brand hype, consider smarter ways to spend your hard-earned money.

Related Questions Answered:

Is a GUESS bag worth ₹6,000? Not when affordable alternatives offer similar quality for less.

How to budget for luxury items in Delhi? Prioritize needs, allocate a small “treat” budget, and explore cost-effective options.

Why My Advice Works: Balancing Self-Care and Generosity

My response on Reddit—donate ₹4,000 to a cause in Delhi and buy a ₹2,000 high-quality bag—offers a practical, value-driven solution. Here’s why it’s the best approach:

Smart Spending on Quality Bags: With ₹2,000, you can find stylish, durable bags on Myntra or Amazon India with five-star ratings. Look for features like water-resistant materials or multiple compartments for daily use in Delhi’s busy lifestyle. For example, a quick search for “best affordable bags for women in India” reveals options from brands like Wildcraft or Baggit, often praised for longevity.

Giving Back in Delhi: Donating ₹4,000 can make a real impact. In Delhi, this amount could buy groceries for a low-income family via NGOs like Goonj or fund school supplies for a child through CRY India. Studies, like one from Nature Communications (2017), show that giving boosts happiness more than material purchases, making this a win-win for your wallet and heart.

Breaking the Brand Trap: My advice to “trash the thought” of a ₹6,000 bag and enjoy a “tapri wali chai” celebrates simple joys over consumerism. It aligns with the growing trend among Gen Z in India to prioritize experiences and social good over status symbols, as seen in posts on X.

Why Other Reddit Responses Miss the Mark

Other responses, like “It’s okay to treat yourself” or “Buy six pairs of footwear,” were well-meaning but less practical:

Encouraging Impulse Buys: Suggesting the bag is “worth it” ignores the user’s guilt and the bag’s questionable value.

Vague or Misaligned Ideas: A “quick tour” or multiple footwear purchases don’t address her need for a practical, guilt-free solution. My advice, by contrast, directly tackles her concerns with a clear, actionable plan.

The Power of Generosity in India’s Capital

Redirecting luxury spending to charity has unique benefits in Delhi. With over 20% of India’s population below the poverty line (World Bank, 2023), ₹4,000 can cover essentials like food or medical supplies for those in need. Local organizations like Smile Foundation make it easy to donate effectively. Plus, giving fosters a sense of community, crucial in a bustling city like Delhi.

Pro Tip: Search for “charities in Delhi” or “how to donate in India” to find trusted NGOs. Many allow online donations, ensuring your money reaches those who need it most.

How to Shop Smart for Bags in Delhi

To find a high-quality ₹2,000 bag:

Check Online Reviews: Use platforms like Flipkart or Myntra, filtering for 4.5+ star ratings.

Visit Local Markets: Places like Sarojini Nagar or Lajpat Nagar offer trendy bags for ₹500–₹2,000.

Prioritize Functionality: Look for durable materials and features suited to Delhi’s weather and commute.

Related Search: “Best affordable bags for women in Delhi” or “where to buy cheap stylish bags in India.”

Spending ₹6,000 on a luxury bag might feel tempting, but it’s rarely worth it when you can get quality for less and make a difference with your money. My Reddit advice—donate ₹4,000 and buy a ₹2,000 bag—offers young professionals in Delhi a way to celebrate their success without guilt. By prioritizing value and generosity, you’ll not only save money but also contribute to a better community. Next time you’re eyeing a luxury item, ask yourself: could this money do more good elsewhere?

Call to Action: Share your thoughts on smart spending in Delhi! Have you found great affordable bags or charities worth supporting? Comment below or check out our guide to budgeting in India for more tips.

Anshu Pathak is a passionate writer and avid reader whose love for stories shapes her world. With a heart full of imagination, she weaves tales that resonate with emotion and depth. When she’s not crafting her next piece, you can find her lost in the pages of a novel, exploring new worlds and perspectives. At Moodframe Space, Anshu shares her creative journey, offering insights, stories, and reflections that inspire and connect with readers everywhere.

Namaskar, Over the last few years, I’ve read almost every book that exists on money and investing, from classic books like Rich Dad Poor Dad to psychology-focused ones like Think and Grow Rich to investing guides like One Up on Wall Street. Coming from a day job in investment banking, some of the things I learned really surprised me because they contradicted what I was taught at work. I’m curious to know if you share the same perspective. Below, I’m breaking down the key things I’ve taken away from all these books, sticking as close as possible to what I’ve learned.

1. Rich Dad Poor Dad: The Classic of Classics

Rich Dad Poor Dad by Robert Kiyosaki is the classic of classics, and I can definitely see why it’s so popular. It covers the foundations for finance and money that we don’t get taught in school. The book’s premise is based around the author’s two dads: his biological dad, who said to get a secure job, take the traditional path, and retire with a pension, and his best friend’s dad, a high school dropout who built a business empire and was all about independent thinking and buying assets that make money for you.

Key Takeaway: Assets put money in your pocket, like investments (stocks, shares, real estate, side hustles, businesses). Liabilities take money out and lose value over time, and you want to avoid those, especially when you’re building yourself up. Thinking of your home as a primary investment makes you buy a bigger house than you need, sucking up money in monthly payments that could’ve been used more profitably elsewhere. Every pound or dollar spent today is one that won’t work for you later, so give each one a purpose, like an employee working for you.

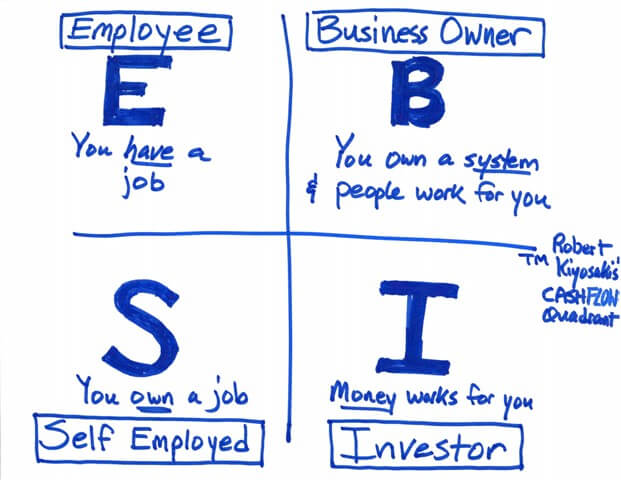

2. Cash Flow Quadrant: Don’t Rely on a 9-to-5

Kiyosaki’s follow-up, Cash Flow Quadrant, shows there are hundreds of ways to earn money beyond a conventional 9-to-5 job. Most people think a stable job is the only legit way to financial security, but this book paints a whole new picture. It makes you understand the limitations of a job and how relying purely on it might just be the worst thing you do for financial freedom.

Key Takeaway: The cash flow quadrant represents four ways to earn money: employee (9-to-5), self-employed (like a dentist or freelancer), big business owner, or investor. The book talks about how to use these paths to achieve financial freedom and which are most likely to get you there. It gets your mind ticking with ideas for earning outside a traditional job.

3. The 4-Hour Workweek: Work Smarter, Not Less

When I saw the title The 4-Hour Workweek by Tim Ferriss, I was skeptical—a four-hour workweek sounded too good to be true. But as I got deeper into the book, I realized it wasn’t about working less; it was purely about working smarter. It shows how anyone can live a retired millionaire lifestyle by building their own business, automating it, and collecting income while living their best life, not waiting years to retire.

Key Takeaway: Something that seems far-fetched is a lot more achievable than you think. Build a business, automate it, and collect income as you go. This book gives you the tools to make the ideas from Cash Flow Quadrant happen, showing you how to earn outside a traditional job setup.

4. The Millionaire Fastlane: Get Rich Quick, But It’s Hard Work

The Millionaire Fastlane by MJ DeMarco says there’s no such thing as get rich easy, but there is such a thing as get rich quick, which is interesting because you don’t hear that often. He talks about three paths: the Sidewalk (spending more than you earn, trapped paycheck to paycheck), the Slow Lane (safe job, saving, retiring at 65+), and the Fast Lane (leveraging time for passive income).

Key Takeaway: The Fast Lane is about investing time in work that generates passive income, like creating a product or system that earns long after your original time investment. It expands your income potential, but MJ keeps it real—it takes hustle, hard work, and discipline. It’s years of experience and knowledge that get you to that “quick” point.

5. Think and Grow Rich: Mindset Is Everything, But…

Think and Grow Rich by Napoleon Hill has people split—you either love it or hate it. Some say it’s all fluff and doesn’t deliver a clear roadmap to wealth, so they’re disappointed. Others say it transformed their mindset and financial lives, like a light bulb moment that helped them unlock limiting money beliefs.

Key Takeaway: Mindset is everything. If you have a scarcity mindset, thinking money’s hard to come by, that’s what you’ll experience. If you believe in abundance and that you’re capable of wealth, your actions align with success. But mindset alone isn’t enough—you need consistent, focused action. If you’re open to digging into your beliefs, this book’s for you; if you want a step-by-step guide, skip it.

6. The Psychology of Money: It’s More Than Math

I have a whole video on The Psychology of Money by Morgan Housel, so I’ll link that here. Money is as much about psychology as it is about math—our feelings, past experiences, and how we perceive money often overshadow raw financial knowledge. The most interesting part is how we misattribute luck in financial lives.

Key Takeaway: We study exceptional success stories like Bill Gates, thinking we can replicate them, but the more exceptional the story, the more luck played a role, and the fewer lessons you can apply. Focus on patterns, not people. Patterns like disciplined saving and investing work for everyone and don’t need luck. I’ve got a free guide on this—page 32 covers proven investing fundamentals, linked in the description.

7. The Intelligent Investor: Keep It Rational

The Intelligent Investor by Benjamin Graham is what Warren Buffett read at 19, and he still calls it the best investing book ever. Its principles are timeless. You don’t need specialist knowledge or deep insight—just two things.

Key Takeaway: Long-term investing needs a rational framework to make decisions and not letting emotions override it. It covers how the market behaves, basic finance fundamentals, and controlling your psychology to stay disciplined.

8. Girls That Invest: Beginner-Friendly Investing

Girls That Invest by my friend Sim is a really good book for the ultimate beginner. It covers why you should invest, the basics and terminology, and how to find your investing personality type.

Key Takeaway: Learn the basics of investing, understand your risk tolerance, and create a portfolio that matches it. This book makes investing approachable for anyone starting out.

9. The Little Book of Common Sense Investing: Index Funds Rule

The Little Book of Common Sense Investing by John Bogle, Vanguard’s CEO who invented index funds, argues that the winning strategy for beginners is simple—invest in index funds indefinitely.

Key Takeaway: Index funds outperform most alternatives because of low costs and broad market exposure. Bogle’s asset allocation (stocks to bonds) is a bit conservative and outdated, so follow up with books like The Dhandho Investor or One Up on Wall Street.

10. The Dhandho Investor and One Up on Wall Street: Invest in What You Know

The Dhandho Investor by Mohnish Pabrai and One Up on Wall Street by Peter Lynch say the best investments are often right under your nose, in things you know and engage with daily. I had Invisalign five years ago, loved the product, researched the company, and bought their stock—it’s my biggest return ever.

Key Takeaway: As a customer, you have an advantage over Wall Street pros by investing in companies you understand, but it’s not just about being a customer—you need to research thoroughly before investing.

11. Ignorance Debt and Investing in Yourself

Alex Hormozi’s concept of “ignorance debt” applies to investing—the difference between where you are and earning millions is just information you haven’t learned yet. Beginners often think they know more than they do, which can mislead them without a strong foundation. Also, most money books don’t mention this, but investing in yourself comes first.

Key Takeaway: Before the stock market, invest in your ability to manage money or make more through a business or side hustle. It’s harder work but more impactful in the short term than the slow game of investing. I’ve got a playlist on this, linked here.

Summary Table: Key Lessons from Money and Investing Books

Book/Concept

Key Lesson

Core Insight

Rich Dad Poor Dad

Assets vs. Liabilities

Buy assets (stocks, real estate, side hustles) that put money in your pocket, avoid liabilities that drain it. Don’t see your home as a primary investment.

Cash Flow Quadrant

Beyond the 9-to-5

Four ways to earn: employee, self-employed, business owner, investor. Move toward business or investing for financial freedom.

The 4-Hour Workweek

Work Smarter, Not Less

Build and automate a business for passive income to live your best life now, not waiting for retirement.

The Millionaire Fastlane

Fast Lane to Wealth

Create passive income systems (products, businesses) with hustle and discipline for quicker wealth-building.

Think and Grow Rich

Mindset + Action

An abundance mindset aligns actions with success, but you need consistent action to make it work.

The Psychology of Money

Focus on Patterns

Exceptional success often involves luck; focus on proven patterns like disciplined saving, not outliers like Bill Gates.

The Intelligent Investor

Rational Investing

Use a rational framework and emotional discipline for long-term investing success, no special knowledge needed.

Girls That Invest

Beginner Investing

Learn investing basics, find your risk tolerance, and build a portfolio that matches your goals.

The Little Book of Common Sense Investing

Index Funds

Invest in index funds for low-cost, effective wealth-building, but consider modern allocation strategies.

The Dhandho Investor / One Up on Wall Street

Invest in What You Know

Invest in familiar companies after thorough research, leveraging your customer experience for an edge.

Ignorance Debt / Invest in Yourself

Learn and Grow

Bridge ignorance with knowledge; invest in your money management and earning skills for faster results.

FAQs

What’s the main lesson from Rich Dad Poor Dad?

It’s about assets (like stocks or side hustles) putting money in your pocket and liabilities (like cars) taking it out. Avoid thinking your home is a primary investment—it can trap your money.

How does Cash Flow Quadrant change your view on jobs?

It shows a 9-to-5 job limits financial freedom. The four ways to earn—employee, self-employed, business owner, investor—push you to explore business or investing for more freedom.

Is The 4-Hour Workweek really about working four hours?

No, it’s about working smarter by building and automating a business to generate passive income, so you can live your dream life now, not after years of waiting.

What’s the “Fast Lane” in The Millionaire Fastlane?

It’s creating passive income systems, like products or businesses, that earn long after your work. It’s “get rich quick” but needs years of hustle and discipline.

Does Think and Grow Rich give a clear wealth plan?

No, it’s about mindset—believing in abundance over scarcity. It helps unlock limiting beliefs but needs action to work, not just positive thinking.

Why focus on patterns in The Psychology of Money?

Exceptional success stories often rely on luck, which you can’t copy. Patterns like disciplined saving and investing are reliable and work for everyone.

Who should read The Intelligent Investor?

Anyone wanting a timeless, rational approach to investing. It teaches a decision-making framework and emotional control, no genius required.

How does Girls That Invest help beginners?

It explains why to invest, basic terms, and how to find your investing personality to build a portfolio that fits you, perfect for newbies.

Why does The Little Book of Common Sense Investing love index funds?

Index funds are low-cost and outperform most options for beginners, but Bogle’s stock-bond allocation might be too conservative, so check other books.

How do I invest in what I know, per One Up on Wall Street?

Use your experience as a customer to spot good companies, like I did with Invisalign, but do deep research before buying their stock.

Why invest in myself before the stock market?

Investing in your money management or earning skills, like starting a side hustle, gives quicker results than the slow game of stock market investing.

Anshu Pathak is a passionate writer and avid reader whose love for stories shapes her world. With a heart full of imagination, she weaves tales that resonate with emotion and depth. When she’s not crafting her next piece, you can find her lost in the pages of a novel, exploring new worlds and perspectives. At Moodframe Space, Anshu shares her creative journey, offering insights, stories, and reflections that inspire and connect with readers everywhere.

Namaskar, After spending a decade diving deep into finance through a degree, accounting qualifications, and a career in investment banking, I’ve learned that mastering personal finances is one of the most life-changing skills you can develop. Recognizing and breaking bad money habits is key to financial freedom. Below, I share nine common bad money habits that hold people back, along with practical tips to overcome them, drawing heavily from insights like those in Robert Kiyosaki’s Rich Dad Poor Dad.

1. Paying Yourself Last

I first heard about this concept in Rich Dad Poor Dad by Robert Kiyosaki, and it’s a blueprint for achieving financial freedom. Poor people’s habit is paying yourself last—when your paycheck arrives, you pay rent, phone bills, subscriptions, and fund social plans, saving whatever’s left (if anything). Rich people do the opposite.

Solution: Pay yourself first. Take a minimum of 10% of your income and put it into a savings account the minute you get paid. Treat it like a bill—it’s that important. This ensures you’re prioritizing your financial future.

2. Getting Comfortable with Bad Debt

Debt is practically the norm these days. People use it for small things—presents, clothes, you name it. My rule? Unless I can pay for something outright in cash, I don’t buy it with debt. Credit card companies want you to be bad with finances because that’s how they make money, with average interest rates at 22%, canceling out any rewards.

Solution: Don’t buy what you can’t afford without debt. If you’re not able to pay off your credit card in full, avoid using it for non-essentials to escape the high-interest trap.

3. Not Building a Financial Buffer

Paying yourself first ties into this. Without a financial buffer, you’re vulnerable to life’s surprises. Saving enough for a six-month buffer through that 10% habit gives you security.

Solution: Start putting that 10% away consistently. Once you have your six-month stockpile, use additional savings to build an investment fund and explore investment options.

4. Not Knowing Your Income or Expenses Properly

Lifestyle inflation is real—your spending rises as your income does. The more you make, the more you spend, like buying a bigger house or car. Without knowing your starting point, how can you plan where you want to be? Financially savvy people know their assets, liabilities, and have clear goals.

Solution: Track your income, expenses, assets, and liabilities. Seeing those numbers in black and white triggers action. Set clear financial goals and outline the steps to get there.

5. Having Expensive Hobbies

A lot of people love to shop, and yeah, it’s fun, but it’s a bad money habit if it’s draining your wallet. To improve your financial position, you need to save more or make more—or ideally both.

Solution: Focus on saving a larger percentage of your income while creating new income streams. You can’t build wealth if you’re spending everything you earn, but saving alone has limits. Balance both sides for real progress.

6. Thinking Saving Alone Builds Wealth

Using cashback sites or cutting expenses only goes so far—there’s a cap to how much you can save. The making-money side, however, is infinite. Wealth-building requires both saving and earning more.

Solution: Break the habit of thinking saving alone will make you rich. Look into investing in the stock market, asking for a pay raise, or starting a side hustle to unlock unlimited earning potential.

7. Paying Too Much in Taxes

Taxes are the single biggest expense in your life. While everyone has to pay them, wealthy people use legal corporate structures or tax advisors to minimize their tax bills.

Solution: Understand tax rules to stack the deck in your favor. Invest through an ISA or Roth IRA to shelter dividends and profits from taxes, or operate as a business for tax advantages. Even if you’re okay paying more taxes, reducing your bill lets you redirect funds to causes you value.

8. Waiting Too Long to Invest

Once you have savings and that emergency buffer, don’t let your money sit in a bank account. Inflation eats away at its value every year, meaning you’re losing money. Waiting too long to invest makes it harder to achieve your goals.

Solution: Start investing once you have your stockpile. Diversify with a mix of safe and riskier investments to weather life’s ups and downs. Don’t leave excess money in a bank account—make it work for you.

9. Not Making Your Money Work for You

There’s always an excuse for not investing—lack of time, money, or knowledge. But the longer you put it off, the harder you’ll have to work for the same results. Your money needs to start working for you.

Solution: Once you’ve saved enough, explore investment strategies. Diversify to handle different economic situations. Don’t let excuses stop you—start small and build from there. Check out resources on investing during tough times, like a recession, to get started.

Summary Table: Bad Money Habits and Solutions

Bad Money Habit

Description

Solution

Paying Yourself Last

Spending your paycheck on bills and expenses before saving, leaving little or nothing to save.

Pay yourself first by transferring at least 10% of your income to savings immediately, treating it like a bill.

Getting Comfortable with Bad Debt

Using credit cards for small purchases, racking up high-interest debt (average 22%).

Only buy what you can pay for outright with cash or debit; avoid credit unless you can pay it off in full.

Not Building a Financial Buffer

Lacking savings for emergencies, making you vulnerable to financial stress.

Save 10% consistently to build a six-month emergency fund, then redirect savings to investments.

Not Knowing Your Income or Expenses

Allowing lifestyle inflation, where spending rises with income, without tracking finances.

Track income, expenses, assets, and liabilities; set clear financial goals to guide your actions.

Having Expensive Hobbies

Spending excessively on hobbies like shopping, draining financial resources.

Save more and create new income streams to enjoy hobbies without compromising financial goals.

Thinking Saving Alone Builds Wealth

Relying only on saving, which has a cap, while ignoring income growth.

Combine saving with earning more through investments, pay raises, or side hustles.

Paying Too Much in Taxes

Overpaying taxes without leveraging legal tax-advantaged options.

Use ISAs, Roth IRAs, or business structures to reduce taxes legally; redirect savings to valued causes.

Waiting Too Long to Invest

Leaving money in a bank account, losing value to inflation.

Start investing after building an emergency fund; diversify to manage risks.

Not Making Your Money Work for You

Delaying investments due to excuses, missing out on compound growth.

Explore investment strategies early, diversify, and start small to let your money grow.

FAQs

What does paying yourself first mean?

It means setting aside at least 10% of your paycheck for savings before paying any bills or expenses, treating it like a priority to secure your financial future.

How do I avoid bad debt?

Only buy what you can pay for outright with cash or debit. Avoid using credit cards for non-essentials unless you can pay off the balance in full to dodge high interest rates.

Why is a six-month financial buffer important?

A six-month emergency fund protects you from unexpected expenses, giving you stability while you focus on building wealth through savings and investments.

How can I track my income and expenses?

List your income, expenses, assets, and liabilities. Use a budgeting app or spreadsheet to monitor them and set clear financial goals to stay on track.

How do I balance expensive hobbies with saving?

Save a larger portion of your income and create additional income streams, like a side hustle, to enjoy hobbies without compromising your financial progress.

Why isn’t saving enough to build wealth?

Saving has a cap, but earning more doesn’t. Combine saving with income-boosting strategies like investing or side hustles to maximize wealth-building potential.

How can I legally reduce my taxes?

Explore tax-advantaged accounts like ISAs or Roth IRAs, or operate as a business for tax benefits. Learn tax rules or consult an advisor to minimize your bill legally.

Why should I start investing early?

Investing early leverages compound growth, making your money work harder. Delaying means you’ll need to work harder to achieve the same financial goals.

Anshu Pathak is a passionate writer and avid reader whose love for stories shapes her world. With a heart full of imagination, she weaves tales that resonate with emotion and depth. When she’s not crafting her next piece, you can find her lost in the pages of a novel, exploring new worlds and perspectives. At Moodframe Space, Anshu shares her creative journey, offering insights, stories, and reflections that inspire and connect with readers everywhere.